By Professor Ba Shusong

(This speech was delivered by Professor Ba Shusong at City University of Hong Kong, the content only represent personal view, do not represent any other personal or organizational position)

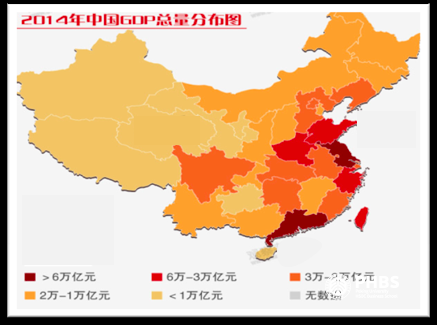

The broad picture behind OBOR, from a global perspective, is about de-leveraging. The percentage of the total global trade in GDP has been decreasing. In recent years, global trade has increased much slower than the general economy and the market consolidation has been going backward, which has innovated China to explore a new area to boost its economy under the new global economic frame. Obviously, the undergoing restructure of global trading frame is mainly amongst US, Europe, and China. Thus, under the current global backdrop, the OBOR is a response to push forward globalization into a new era. To look at the domestic market of China, we see the levels of development of the region vary and are represented by different shades in Figure 1. If you travel to China a lot, it is not hard to find that there are only a few cities developed well like Shenzhen, Bohai bay area and coastal cities alongside that are represented in a deep shade in this picture. The GDP of Guangdong province is almost equivalent to the GDP of the whole of Russia; however, many mid-west regions in China have relatively slow development of economy. So, there is a lack of balance of regional economic development in China, to which a solution for stimulation needs to be found.

Figure 1: The GDP distribution of China in 2014

I have been working in Beijing for more than twenty years. If you drive from the city all the way to its directions of east, west, south or north for two hours, you will find that the suburban areas are very different from the unban areas. Generally speaking, the OBOR policy could bring the development from downstream to the upstream where the economic development is relatively weak. Strategically speaking, internally, it advances the balance of economic development across the nation. On the other hand, to look at the Chinese export, as a giant manufacturer, China traded with its competitive products of living necessities, which are in high demand under the OBOR countries.

China is pushing its currency, RMB, into the global market; and China will have more balanced power on the valuation when it comes to exporting its capital and production capacity. My colleagues from Hong Kong always make jokes about how much they get lost about what is included into the OBOR and what is not, given the policy covers a wide range of industries and aspects. Anyways, to my understanding, the OBOR is basically to reconnect the Euroasia and connect Southeast Asia to Europe through the maritime route. Generally speaking, the economic strength of the countries under the OBOR is in a leading role. We have collected statistics on the development of several regions along the silk road, and it showed that most of the countries have great economic growth potential. Also, the economic diversity among the 60 countries along the silk road is very good, however, there are huge gaps among these economics as well. Since the implementation of the OBOR policy in these countries, there is indeed a progress we can see.

Looking at the investment overseas, in 2016 China overseas investment has reached US$170 billion, which exceeded a trillion RMB. China’s direct investment to the OBOR countries reached US$14.5 billion. Chinese enterprises have established 56 trade co-operation zones in more than 20 OBOR countries with accumulated investment over US$18.5 billion. However, regarding trade, the growth rate actually slows down, but with a stronger economic tie with OBOR countries. For the economic connections, China has signed “The Junker Investment Plan” with the European Union, “The Prairie Road Plan” with Mongolia, “The Four Corner Strategic Plan” with Cambodia, etc. China has also successfully completed the ASEAN Free Trade Zone upgrade negotiation, pushed forward the Maldives Free Trade Zone negotiation with several already on-going financial cooperation, including, first meeting of the East Asian and the Pacific Central Bank Chairman Committee and EMEA organization and ASEAN and China, South Korea and Japan regional cooperation. For regional communication, the number of AIIB members has reached 70. In 2016, the AIIB has made US$1.2 billion investment. We have conducted a report on the projects the AIIB has invested in and found out that AIIB has moved from theories and strategies, to detailed systematic investment operation.

The People’s Bank of China, the central bank, has signed RMB clearance agreement with Vietnam, Mongolia, Laos, Nepal, Kyrgyzstan, North Korea, Kazakhstan, Russia, and Belarus. From 2014 to 2016, China has signed currency exchange agreement with more than 20 countries included in OBOR. By the end of September 2016, offshore currency bureaus have used 21.99 billion Yuan of the surplus of the offshore RMB reserve and the central bank used around US$1.36 billion equivalent from offshore RMB reserve, which stimulated the bilateral trade very well. The interactions between Chinese currency and foreign currencies have become more active than ever before. On the other hand, the People’s Bank of China is pushing forward the direct trading market for Chinese currency. Until the third quarter of 2016, within the bank currency basket, RMB can be traded directly with 17 foreign currencies including Singapore dollar, Malaysian ringgits, Russian rubles, Korean won, UAE dirham, and Saudi riyal. For the open capital market, free-trade zones directly connect with onshore markets included in OBOR.

From the aspect of the current Chinese policy, the RMB internationalization is one of the key points for the OBOR, and how to broaden the use of RMB in the global market is for the following consideration. Amongst the economies under the OBOR, in the manufacturing and industrial zones and free trade zones, the loan of RMB is the major direct investment tool and the silk road economic zone can help to push it much further within Asia. In terms of currency exchange and broadening its scale, China has signed bilateral currency exchange agreement with Kazakhstan’s and Uzbekistan’s central bank. As for the cross-border financial channel broadening, among 14 global clearance banks, seven are OBOR member countries, which support the functions of pricing, clearing, and investment of RMB. Also, this could change the offshore RMB market and make it grow under the OBOR.

There is a point worth mentioning that China brought projects from free trade zones to the OBOR countries, which also connect many Chinese cities to markets under the OBOR. The Chinese also pushed forward the OBOR by establishing financial institutions, for instance the AIIB, the Silk Road fund, etc. In fact, some commercial banks also made structural changes accordingly. In Hong Kong, Bank of China (BOC) sold its Southeast Asian branches to BOCHK, which is made into a subsidiary of BOC so that Hong Kong can participate in the OBOR as synergy and turn the management into regional rather than international. Many other commercial banks followed the same pattern.

From the outside demand, we have seen many projections. The fund for the OBOR is not enough for the growth of the need for investment. A simple prediction is that if within the region the investment increases 40%, then by 2040 new demand for funding would reach US$1 trillion. Hence, the huge funding demand would be a great stimulation to the global financial industry.

From the projects list of the OBOR, we can see that infrastructure projects are priorities including eight railroad projects, five highway projects, two water transportation projects, two pipeline and underground cable projects, and six optical cable projects. The connections of these infrastructures are the priorities of the OBOR.

For the choices of industries for investment, it is well manifested by the demand and capabilities of China and the OBOR countries. First, it is infrastructure, these member countries are very less developed at transportation, electricity, and information technology. Second, it is energy industry and mineral resources exploration. Currently, among the 15 richest oil reserve countries, ten of them are in Eurasia and Africa. 80% of the global oil reserve is located in Eurasia and Africa and 90% of the oil drilling wells are located in these two areas. In the past, resource exploration in developing countries largely relied upon developed countries for both technology and capital. However, China is catching up quickly in terms of technology and capital. The third, airports, seaports, and industrial zone. I have a student who was sent to Belarus by our government to initiate an industrial zone so that Chinese industrial companies can better cooperate with the upstream to make raw material development, distribution and sales efficiently and at low cost. The investment inside the industrial zone has exceeded US$8 billion.

Taking out Europe and America, most of the countries along the Silk Road maritime route including Southeast Asia, South Asia, Middle East and Africa are lack of compatible shipbuilding capability. In this area, China has been growing rapidly in recent years. China not only had its own shipbuilding technology enhanced, but it also invested and established overseas factories to export its technology to other countries. The fifth point, the cultural exchange, which is also the biggest challenge I believe. For example, imagine how hard it would be to find a pop song that is popular in all OBOR countries and can be sung by all the people. However, on the other hand it reflected the diversity as well. Cultural diversity provides a great opportunity to develop cultural tourism, so there is a huge space for cultural tourism to grow. Sixth, agriculture and logistics. The radiation areas of the OBOR are mainly developing countries, so there is a great demand for agriculture and logistics. There are groups of numbers provided by the Department of Commerce. In the first quarter of 2017, Chinese enterprises’ direct investment overseas reached US$20.5 billion, with an obvious decrease of 48.8%, but the direct investment in OBOR countries has reached US$2.9 billion with an increase of 14.4%. 952 contracting agreements with 61 OBOR countries were signed with US$14.4 billion revenue in total. It has become clearer that our overseas free trade zones are getting more effective with implementation of the OBOR policy. In the year of 2016, Chinese enterprises have established 56 free trade zones along the Silk Road with accumulated US$18.5 billion, established 1,082 companies in these free trade zones, created total value of US$ 50.6 billion, paid US$1.7 billion in tax, and created 177000 jobs for the locals and these are only the results have seeing so far. Next, let me go through the major point countries and industrial zones under the OBOR. In regions like Kazakhstan, Uzbekistan, Southeast Asia, Middle East, and the old USSR, the OBOR policy has been well implemented from just a blueprint. We have also seen strategic trade promotions, capital operation, financial institutions cooperation, and the China development bank has worked actively in industrial and financial synergies and China Import-Export Bank, the Silk Road fund also participated by providing more bridging functions. The AIIB, the Silk Road fund, the BRICS Bank, Shanghai Cooperation Organization, and the China Import-Export Bank have all played important roles in building up the financial infrastructures to support OBOR.

Speaking of Hong Kong, geographically it is linked with the OBOR economies. Financially, the demand for funding is rising and within the OBOR region there are two international financial centers, London and Hong Kong. As we talked above, Hong Kong is a key financial center in Asia, thus there is greater space for Hong Kong to enhance its status in the OBOR. Based on the observation of the market, Secretary Leung just talked a lot about equity funding, especially growth funds and companies that brought changes to the regulation system and the market structure to better adapt to the new economic environment.

In fact, for now, there is a space for strategic market to grow. The strategic market is not very well developed for Hong Kong, but actually there is great need for that. Prime Minister Li Keqiang, during the two sessions of National People’s Congress (NPC) and Chinese People’s Political Consultative Conference (CPPCC), announced the start of securities connection since the Shanghai-Hong Kong Stock Connect and Shenzhen-Hong Kong Stock Connect were launched. The securities connection is basically to connect Hong Kong and foreign investment companies to the mainland market up north. Mainland capital investment to offshore can boost the Hong Kong securities market. For now, we can see a great demand in the market.

The regulation department has paid attention to the Panda Bonds market. In 2016, besides simplifying the regulation and bureaucratic process, the central bank clearly stated that if the Panda Bonds can use its raised capital in the subsidiary companies of the Chinese companies onshore, then the external debt limit will be lifted for it. In last month, BOC successfully completed its pricing of US$3 billion equivalent bond issuing, and it will be listed on the Hong Kong Stock Exchange and the capital raised will be used for OBOR investment projects.

The first offshore RMB bond-rainbow in Africa was issued by BOC Johannesburg, issuing size was 1.5 billion Yuan, and is also applicable for projects under the OBOR. Hong Kong could play an essential part in the same kind of work. The issuing of the panda bond and rainbow bond largely supported the AIIB, the Silk Road fund, and BRICS Bank on infrastructure investment and also supported the offshore bond market momentum. Since the RMB exchange rate reform in August 2015, recently there appeared pressure for RMB to devaluate given a strong US dollar at that time. Thus, from a global perspective, the offshore RMB pool scale is actually decreasing for the Hong Kong, London, and Singapore market.

Hong Kong is the largest offshore RMB center, with its peak which once reached 1 trillion RMB and now decreased to 500 billion RMB. This market is now shrunk, and a slow down can be observed in the use of RMB to price in global trade. Objectively speaking, RMB needs to transfer its pricing function to investment, credit, and risk management. Actually, we all learned about RMB‘s inclusion into the IMF’s special drawings rights (SDR), and it is the first emerging market currency to be included in the SDR with a 10.19% share. So calculated with a 10.19% substitute in the IMF formula, resulted in 10% of pricing and use of the currency. However, there is only less than 1% of financial products priced in RMB. Now, the global trade is slowing down and the internationalization path of RMB switched from pricing to investment, credit, and risk management. For example, to complete the clearing system and develop RMB-denominated financial instruments. Since 2016, HKEX developed CNH futures and CNH options which are well welcomed by the market.

Meanwhile, the question is; how to broaden the market for using RMB through RMB-denominated instruments? To explore some of the specific regions under the OBOR, Hong Kong as a free trade and international financial center has a lot to do to increase its competitiveness. Also, with connection to the Mainland stock markets, we are exploring how to make Hong Kong an asset management center for the entire OBOR.

Onshore market currently still has rather restrictive capital regulation, while Hong Kong is a rather open and free market. The connection can only make trades more active with many conditions, for example, to invest in two markets in two regions the investor has to learn about the two markets so that different supplies and demands can be matched. In fact, TWSE and SGX also made similar initiatives, and to activate it, tens of millions of Taiwanese dollars to be spent but probably with only several hundreds of thousands of deals could be made. The same happened to SGX in the past.

Timezone difference also needs to be taken into account. If there is a timezone difference and capital flow crossing border can only happen during overlapped market hours, the number of deals could be very small under the connectivity programme. We see the success of Shanghai-Hong Kong Stock Connect and Shenzhen-Hong Kong Stock Connect, but there are many other connectivity programme that did not go very well. After the activation, the next step is to spread it to bond markets connection and other kinds of connection as well, which supplies a better opportunity for asset management, and with the volatility of the RMB market in Hong Kong and sharp increase of the RMB scale aftermath in Hong Kong, there is actually an arbitrage space for the Hong Kong market. With the two directional volatility of the currency, there are many interest arbitrage spaces so once the internationalization of RMB is realized, there needs to be more stable products to rely on. Thus interest arbitrage is not enough because any cities with active offshore RMB business can do. So it is necessary for RMB to transfer to financial products from pricing, and which can only make the financial center last long.

We all know that Hong Kong is a traditional shipping center even though it was heavily hit by the opening of many ports in the mainland, Hong Kong still plays an important role in global shipping logistics. How to influence and develop trades and shipping financial products and services of maritime legislation and arbitration within Hong Kong, Macau and Taiwan need consolidation. There is actually in great need.

Hong Kong could also play an significant role in providing intermediary services and financial advice for infrastructure investment projects along the Silk Road, for example to offer investment risk management services. Various intermediary transfer and relevant expertise can be a great advantage for Hong Kong to participate in the OBOR.

Prof. Ba Shusong

Managing Director, Chief China Economist, HKEX

Chief Economist, the CBA

Executive Director, the HSBC Financial Research Institute at Peking University

Prof. Ba Shusong

Managing Director, Chief China Economist, HKEX

Chief Economist, the CBA

Executive Director, the HSBC Financial Research Institute at Peking University

Professor Ba Shusong is Managing Director, Chief China Economist of Hong Kong Exchanges and Clearing Limited (HKEX), Chief Economist of the China Banking Association (CBA) and Executive Director of the HSBC Financial Research Institute at Peking University. He is also Deputy Secretary General of the China Society of Macroeconomics, a member of Ministry of Commerce's Economic and Trade Policy Advisory Committee, a member of China Banking and Insurance Regulatory Commission’s Expert Guidance Committee for the banking industry’s implementation of the new Basel capital accord, a member of China Securities Regulatory Commission’s M&A Specialists Committee, a member of China’s “13th Five-Year Plan” National Development and Planning Specialists Committee, and Director-General of Peikang Chang Research Foundation of Development Economics.

Professor Ba is a fellow of experts who receive the State Council’s special allowance. He was previously Deputy General Manager of the Bank of China Hangzhou Branch, Assistant General Manager of Bank of China (Hong Kong), Director-General of the Strategy and Development Committee of the Securities Association of China, and Deputy Director-General of the Financial Research Institute of the State Council's Development Research Centre. He was engaged in post-doctoral research in the China Center for Economic Research at Peking University and was a senior visiting scholar at Columbia Business School. He also served as the chief expert in the basic research field of "International Economic and Financial Structure" in Development Research Center of the State Council. Professor Ba was awarded by China’s Social Science Assessment in 2017 as the Chinese scholar with the highest citation frequency in Chinese literature on economics from 2006 to 2015.

Professor Ba had participated in a large number of seminars and forums held by policy-makers in the financial fields as a financial specialist, and lectured to members of the Political Bureau of the CPC Central Committee in China as the main speaker. He had held management positions in a wide range of financial institutions including commercial banks, securities companies, public funds and trust companies. As an expert who is familiar with the actual practice of China's financial operations and policy-making process as well as well versed in financial theory research, he possesses rich practical experience and research achievements in the fields of the Basel capital accord and risk management, asset management (has published an annual report on China’s asset management industry development in 11 consecutive years), banking development and bankers survey (has led the conduction and publication of the annual bankers survey reports in Chinese and English for 8 years), etc. His publications (in Chinese) include "Research on New Basel Capital Accord", "Basel II in Financial Crisis: Challenges and Improvements", “Study on Basel Capital Accord III”, “Basel III and Financial Regulatory Reform”, “Annual report of China Asset Management Industry Development". Professor Ba received the Global Youth Leader Award from the World Economic Forum in 2009.

Edited by Sophie Wu