The 8th PKU-NUS Annual International Conference on Quantitative Finance and Economics was held at the Suzhou Research Institute of National University of Singapore (NUS) from May 18 to 19, 2024. Jointly organized by the Risk Management Institute (RMI) of the National University of Singapore (NUS), Peking University HSBC Business School (PHBS), and the Key Laboratory of Mathematical Economics and Quantitative Finance of the Ministry of Education at Peking University (PKU), this year’s conference attracted nearly 200 scholars to attend online and onsite, sharing the latest research findings in the field of quantitative finance and economics.

A group photo of participants

From left to right, Professor Chen Yi-Chun, director of RMI at NUS , Associate Professor Cheng Xue from the Department of Financial Mathematics of the School of Mathematical Sciences at PKU, and PHBS tenured Associate Professor Peng Xianhua.

In his speech, Professor Chen Yi-Chun reviewed the history of the PKU-NUS Conference and welcomed the participants, expressing hope for continued cooperation between PKU and NUS. Professor Cheng Xue introduced the research trends of the Key Laboratory of Quantitative Economics and Mathematical Finance, hoping that this conference could promote more in-depth and extensive exchanges and cooperation. Professor Peng Xianhua expressed his gratitude to the co-organizers, reviewed the academic achievements of PHBS in 2023, and hoped that this event could enhance the communication and friendship between the scholars.

This year’s keynote speakers included Kay Giesecke, the founder of the Advanced Financial Technology Lab at Stanford University, director of the Mathematical and Computational Finance Program, and Professor at the Institute for Computational and Mathematical Engineering; Wang Neng, chair professor of finance at Columbia Business School, and Ciamac C. Moallemi, chair professor in the Department of Decision, Risk, and Operations at Columbia Business School.

Professor Kay Giesecke gave a keynote speech online

Professor Kay Giesecke delivered a keynote on "AICO: Model-Agnostic Feature Significance Testing for Supervised Learning." Although machine learning has been increasingly used for screening and decision making in many fields, the opaqueness of machine learning limited its adoption in highly regulted fields requiring transparency such as healthcare and financial services. To address this, he introduced AICO (Add In Covariates), a new model-agnostic hypothesis testing framework. AICO defines the baseline sample as the sample with all features being equal to their mean values respectively and then defines the effect of a feature as the improvement of score value when the feature in the baseline sample is changed to the true feature value. Based on the defined feature effect, AICO provides interpretable measures of feature importance with confidence intervals. Its advantages include flexibility in model specifications and scalability to high-dimensional features. He illustrated AICO's effectiveness in handling discrete, non-normal, correlated features and classification tasks, comparing it to Shapley value, deep model-X knockoffs, and holdout randomization tests. He emphasized AICO's low computational requirements and broad applicability, including in mortgage risk, real estate pricing, and climate financial risk assessments.

Professor Wang Neng presented his study

Professor Wang Neng presented his study on the "Economics of Dynamic Capital Structure," focusing on the core of finance: capital structure comprising project, debt, and equity. Despite extensive research, capital structure literature often overestimates leverage ratios compared to actual data. Drawing from Graham's survey, firms link financial flexibility to debt decisions. Professor Wang proposed an integrated dynamic framework that combines the Tradeoff Theory and the Pecking-Order Hypothesis into a financial-flexibility model. Specifically, he developed a time-variant dynamic tradeoff theory, simulating debt prices through Markov Subgame Perfect Equilibrium. Incorporating costly external equity, he explained the origin of adverse selection. Treating debt as a state variable, he highlighted firms' need for financial flexibility, justifying the value of equity issuance delays. Lastly, he revealed that higher equity financing costs paradoxically lead to lower leverage due to the higher value of financial flexibility.

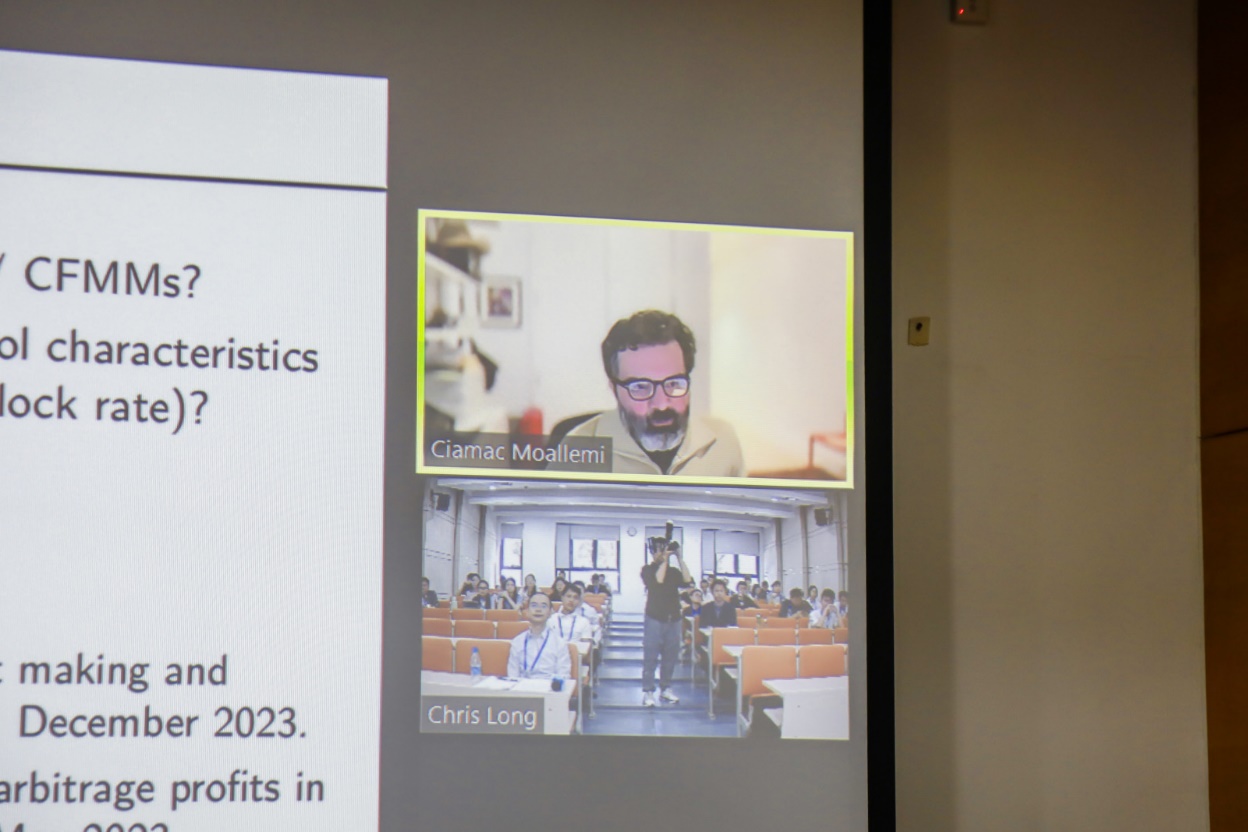

Professor Ciamac C. Moallemi shared his insights with participants

Professor Ciamac C. Moallemi gave a keynote speech on “The Economics of Automated Market Making and Decentralized Exchanges.” The automated market making (AMM) protocols, such as Uniswap have emerged as an efficient alternative to traditional central limit order books, eliminating the need for active intermediaries. Consequently, AMMs become the dominant market mechanism for trust-less decentralized exchanges (DEXs) on blockchain platforms like Ethereum, with Uniswap's trading volume surpassing that of Coinbase. Professor Moallemi and his co-authors developed a model exploring AMMs' economics from the perspective of passive liquidity providers (LPs), introducing a "Black-Scholes formula for AMMs." They considered LP returns post-market risk hedging and identified the main adverse selection cost, 'loss-versus-rebalancing' (LVR). In a Black-Scholes framework, they derived the closed-form expression for this cost. Their model highlights factors driving AMM LP returns, including asset characteristics (volatility), AMM characteristics (curvature/marginal liquidity), and blockchain characteristics. Their model’s expressions accurately match Uniswap v2 WETH-USDC trading pair's LP returns, providing insights into AMM LP investment decisions.

Scholars at the annual conference

Other scholars presenting papers came from world-renowned universities and institutions, including the University of Texas at Dallas, the National University of Singapore, Peking University, the Hong Kong University of Science and Technology, the Chinese University of Hong Kong, the City University of Hong Kong, Hong Kong Polytechnic University, the Renmin University of China, Fudan University, Wuhan University, Tongji University, and Soochow University. Eight faculty members and students from PHBS, including Peng Xianhua, Seungjoon Oh, Yang Aoxiang, Zhao Lingxiao, Shen Chao, Liu Yifu, Zhan Xingyi, and Xu Weixi, presented their papers and shared their recent research findings with attendees.

Initiated in 2016, the PKU-NUS Annual International Conference on Quantitative Finance and Economics has been held to provide a platform for researchers and practitioners from academia and industry to discuss and exchange ideas on the new developments in quantitative economics and finance.

By Annie Jin, Liu Yifu, Zhan Xingyi, and Xu Weixi

Source: Research Office and PR & Media Office