On August 30, the Advanced Macro Workshop on Control Theory and Infinite Dimensional Analysis was held at Peking University HSBC Business School (PHBS), co-hosted by the Sargent Institute of Quantitative Economics and Finance (SIQEF) at PHBS, Institute for Advanced Study (IAS) and Economics and Management School at Wuhan University, as well as the University of International Business and Economics. During the event, more than 40 scholars from China and abroad participated in discussions on the latest academic research in the field of control theory and infinite dimensional analysis.

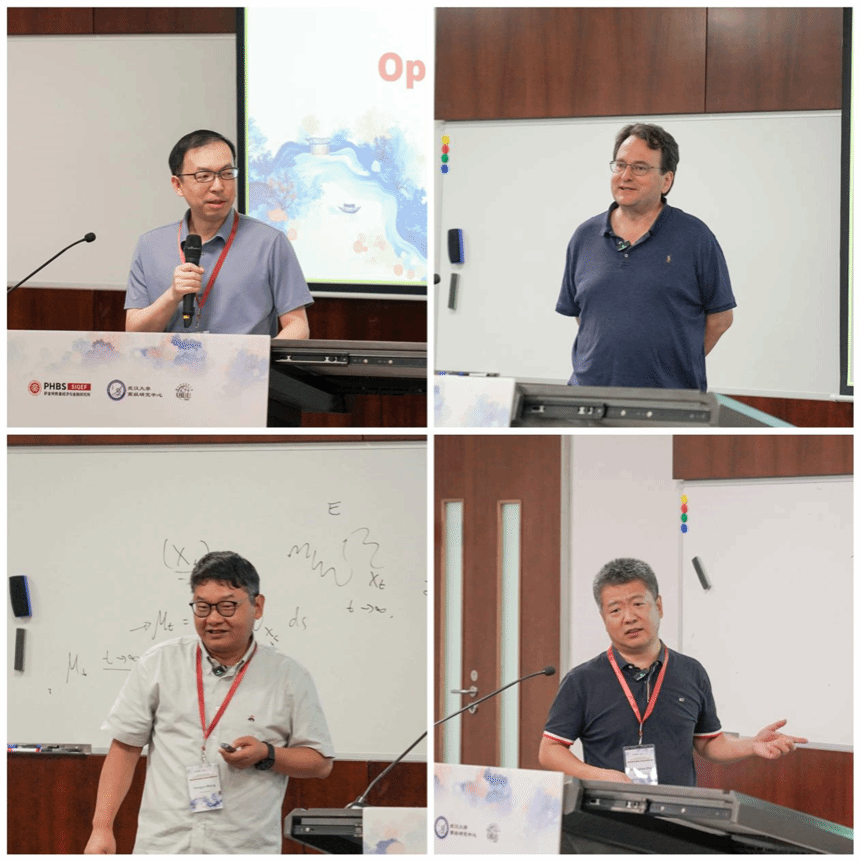

From left to right and top to bottom:Nie Jun、Felix Kübler、Wang Fengyu、Zhu Shenghao

Professor Nie Jun from Wuhan University presided over the opening ceremony. He stated that the conference aimed to promote interdisciplinary research between mathematics and economics to address computational challenges in high-dimensional economic models. Professor Nie reviewed the achievements of previous workshops and briefly introduced the agenda, which includes three economics papers and four mathematics papers, emphasizing the importance of cross-disciplinary dialogue in advancing frontier macroeconomics research.

Professor Felix Kubler from the University of Zurich and fellow of the Econometric Society, presented the paper titled “Deep uncertainty quantification: with an application to integrated assessment models." In the context of climate-economic modeling, the study proposed combining deep neural networks and Gaussian processes to build surrogate models for quantifying uncertainty in high-dimensional parameter spaces. Through computational experiments and Bayesian quadrature methods, the sensitivity of the social cost of carbon to key parameters was analyzed. Results showed that discount rates, risk aversion, and elasticity of substitution significantly could affect carbon costs, while mitigation cost parameters played a minor role.

Professor Wang Fengyu from Tianjin University presented the paper, “Spectral Representations on Wasserstein Limits of Empirical Measures on Manifolds.” In the context of studying the convergence of empirical measures for diffusion and Markov processes, the paper proposed an analytical method based on spectral representations and Dirichlet eigenvalues. Employing coupling, heat kernel estimation, and Wasserstein distance theory, the paper investigated the convergence rate of empirical measures under Wasserstein distance and its relationship to the manifold dimension. The results showed that the convergence rate could strongly depend on the dimension and revealed the accelerating effect of divergence-free perturbations on convergence.

Professor Zhu Shenghao of the University of International Business and Economics presented the paper titled “Stability of a Heterogeneous Agent Model with Human Capital,” which investigated whether a heterogeneous-agent economy can converge to a stationary equilibrium. The paper proposed using relative entropy and the McKean-Vlasov SDE framework to study this stability issue. By constructing a dynamic model that incorporates incomplete markets and human capital accumulation risk, the study examined the conditions for convergence of human capital distribution and derives the existence and convergence rate of the stationary distribution. It revealed that the distribution of the economic system could converge to a stationary state under certain conditions.

From left to right and top to bottom:Liu Wei, Mou Chenchen, Wei Xiaoli, and Serguei Maliar

Professor Liu Wei from Wuhan University presented the paper, “Concentration Inequalities and Exponential Convergence for Mean-Field interacting Particle Systems and McKean–Vlasov Equation.” Within the study of mean-field particle systems and McKean–Vlasov dynamics, he noted that under a weak interaction condition one could bypass convexity and obtain explicit, computable bounds. Using coupling (approximate componentwise reflection), functional inequalities, Euler–Maruyama schemes, and propagation of chaos, the work analyzed links among convergence, bias, and pathwise concentration.

Associate Professor Mou Chenchen from City University of Hong Kong presented a paper titled “On Well-posedness of Mean Field Game Master Equations: A Unified Approach.” In the context of mean field games with common noise, this study introduced a necessary and sufficient Lipschitz continuity condition. Using the FBSPDE system, semi-monotonicity analysis, and tensor Γ mapping methods, the paper investigated the relationship between the existence, uniqueness, and monotonicity of the solutions to the master equation. The results showed that under certain semi-monotonicity conditions, the master equation is also globally well-posed. The study also explored applications to potential games, finite state models, and minimax solutions in nonmonotonic situations.

Associate Professor Wei Xiaoli from Harbin Institute of Technology presented the paper titled “Unified Continuous-time q-learning for Mean-field Game and Mean-field Control Problems.” Addressing mean-field games and control problems, the study introduced a unified q-learning framework using decoupled value functions for agent-population interactions, with policies learned via martingale conditions. Parametrized functions (e.g., neural networks) and numerical simulations were applied to financial models like wealth processes. The Results confirmed effective equilibrium policy learning and numerical convergence.

Professor Serguei Maliar from Santa Clara University presented the paper titled "Hierarchical Reinforcement Learning for Dynamic Economic Models". To address computational challenges in high-dimensional state spaces, the study developed an HRL framework: low-level policies manage local states (e.g., provincial economies) while high-level policies coordinate global objectives. Using neural networks for policy parameterization with experience replay and stochastic gradient descent, the method was applied to heterogeneous-agent models like Krusell-Smith. Results demonstrated significant mitigation of the curse of dimensionality and enhanced efficiency in large-scale policy simulations.

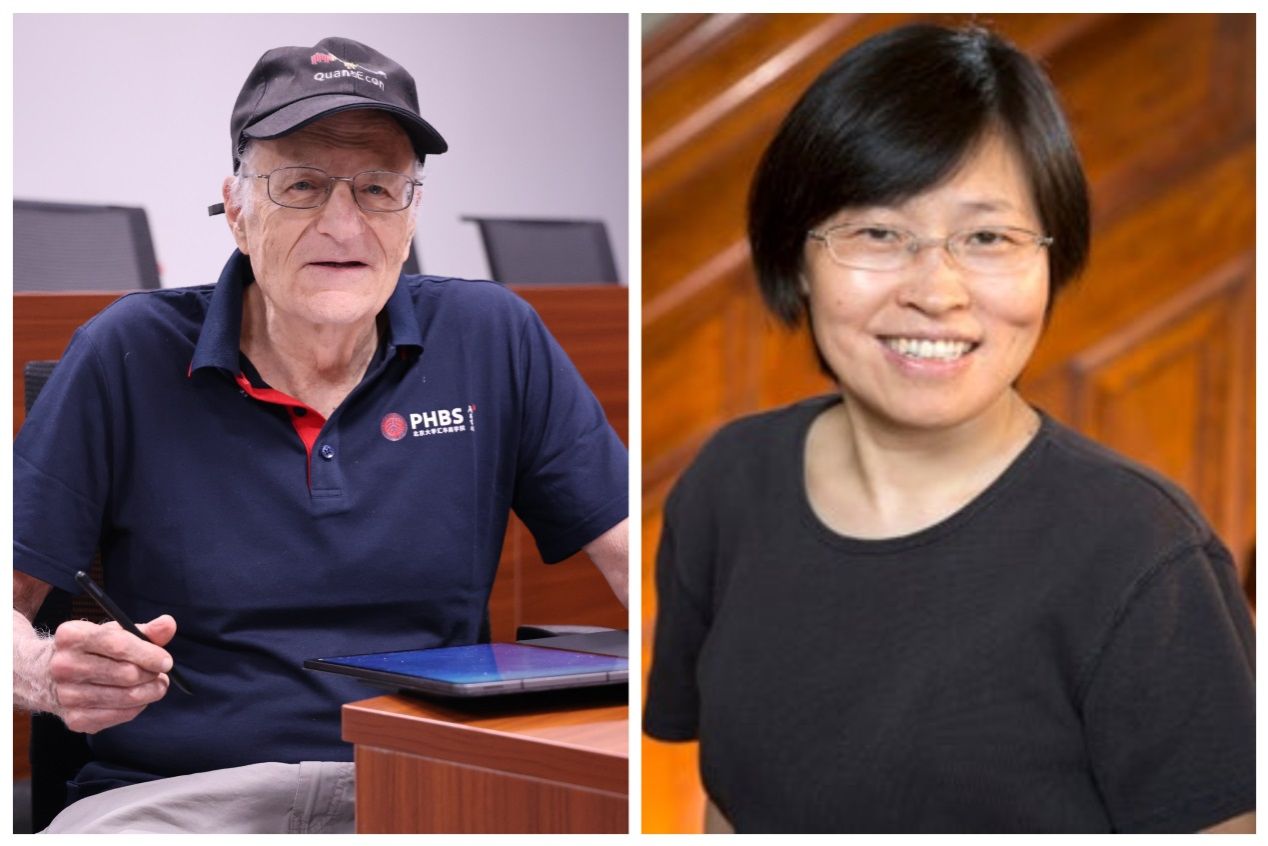

From left to right:Thomas J. Sargent and Chen Xiaohong

This workshop was honored to have the guidance throughout by Professor Thomas J. Sargent, the 2011 Nobel laurate in economics and honorary director of the Sargent Institute of Quantitative Economics and Finance at PHBS. Professor Chen Xiaohong, fellow of the American Academy of Arts and Sciences, fellow of the Econometric Society, and Malcolm K. Brachman professor of economics at Yale University, also participated in the full event via online connection.

The group photo of participants

In 2024, SIQEF was designated as a "Shenzhen Key Research Base in Humanities and Social Sciences" (Funding Category). This event received support from this designation, as well as from the Key Project of the National Natural Science Foundation of China "Machine Learning Algorithms for Solving and Applications of Heterogeneous Dynamic Macro Models" (72433004) and the Original Exploration Program Project of the National Natural Science Foundation of China "A New Generation of Macroeconomic Large Models Based on Infinite-Dimensional Dynamic Control and Artificial Intelligence" (72450003). This workshop not only showcased high-level cutting-edge research but also strengthened interdisciplinary and international academic exchange, injecting new momentum into the in-depth development of macroeconomics in areas such as optimal control and high-dimensional analysis.

By Chen Chenxuan, He Pengyu, Su Chenyu, Wu Qianfeng, Yan Xihe, and Annie Jin

From SIQEF and PR & Media Office