In many countries, student loans are very important for financing higher education. As such, the policy is often seen as a way of improving access of students to education, especially for those from disadvantaged backgrounds. However, investments in higher education can be risky, e.g. due to uncertainty about successful college graduation and about potential future income. In the US, the level of outstanding student debt is currently close to $1.8 trillion and almost half of all college students drop out of school before earning a bachelor's degree. Trying to address the dropout issue, the US government reformed the higher education finance system in 2009 by introducing a major program of income contingent loans.

In their recent paper, "College Education and Income Contingent Loans in Equilibrium," published in the

Journal of Monetary Economics, Karol Mazur, assistant professor of economics at Peking University HSBC Business School, and Kazushige Matsuda, associate professor of economics at Kobe University in Japan, examine the welfare effects of this reform in a quantitative economy with moral hazard, endogenous selection, general equilibrium, and incomplete markets.

The study shows that the implementation of an income-contingent loan policy in the US has reduced the risks associated with student debt repayment, and consequently, with enrolling into college. As such, the reform has increased the enrollment rate by about 5% and the graduation rate by about 2%. Importantly, it turns out that the moral hazard (due to the insurance eroding incentives for studying in college or providing labor supply after it) and adverse selection (due to attracting lower ability students to enroll into college) induced by this policy in equilibrium are of secondary importance. Intuitively, moral hazard is mild because it is largely dominated by market incentives embedded in the significant wage premium that is available upon successful college graduation (currently about 190%). Similarly, adverse selection is non-existent as there is excess demand for additional human capital due to the lack of insurance contracts for college dropouts and income shocks. Relatedly, as the policy increases the equilibrium supply of human capital for production, the reform is almost self-financing, requiring only very small tax increases.

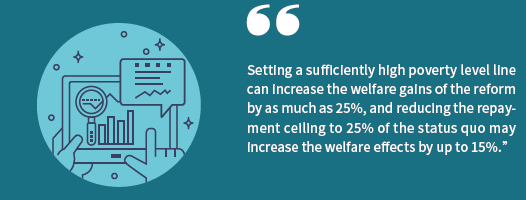

The study also finds that the endogeneity of the skill premium slightly increases the policy’s effectiveness. Finally, Mazur and his coauthor examine how the parameters of the income-contingent loan program affect its welfare implications. For instance, they show that setting a sufficiently high poverty level line can increase the welfare gains of the reform by as much as 25%, and reducing the repayment ceiling to 25% of the status quo may increase the welfare effects by up to 15%.

Overall, the welfare gains associated with the reform introduced in 2009 by the US government are equivalent to a lifetime consumption increase of about 1% for the average member of society. Results of this research suggest that income-contingent loans not only stimulate the equality of opportunity, but also improve both economic efficiency and social insurance.